Principal

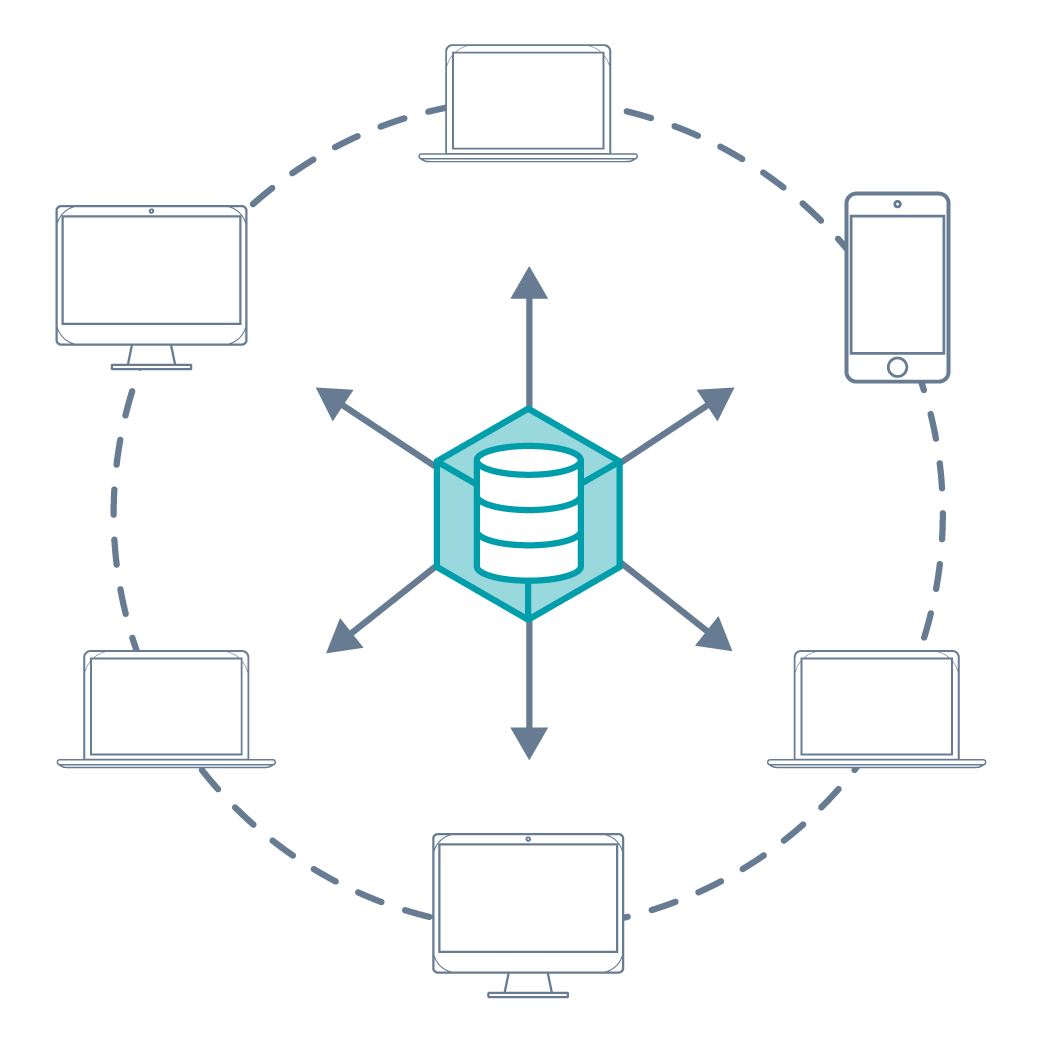

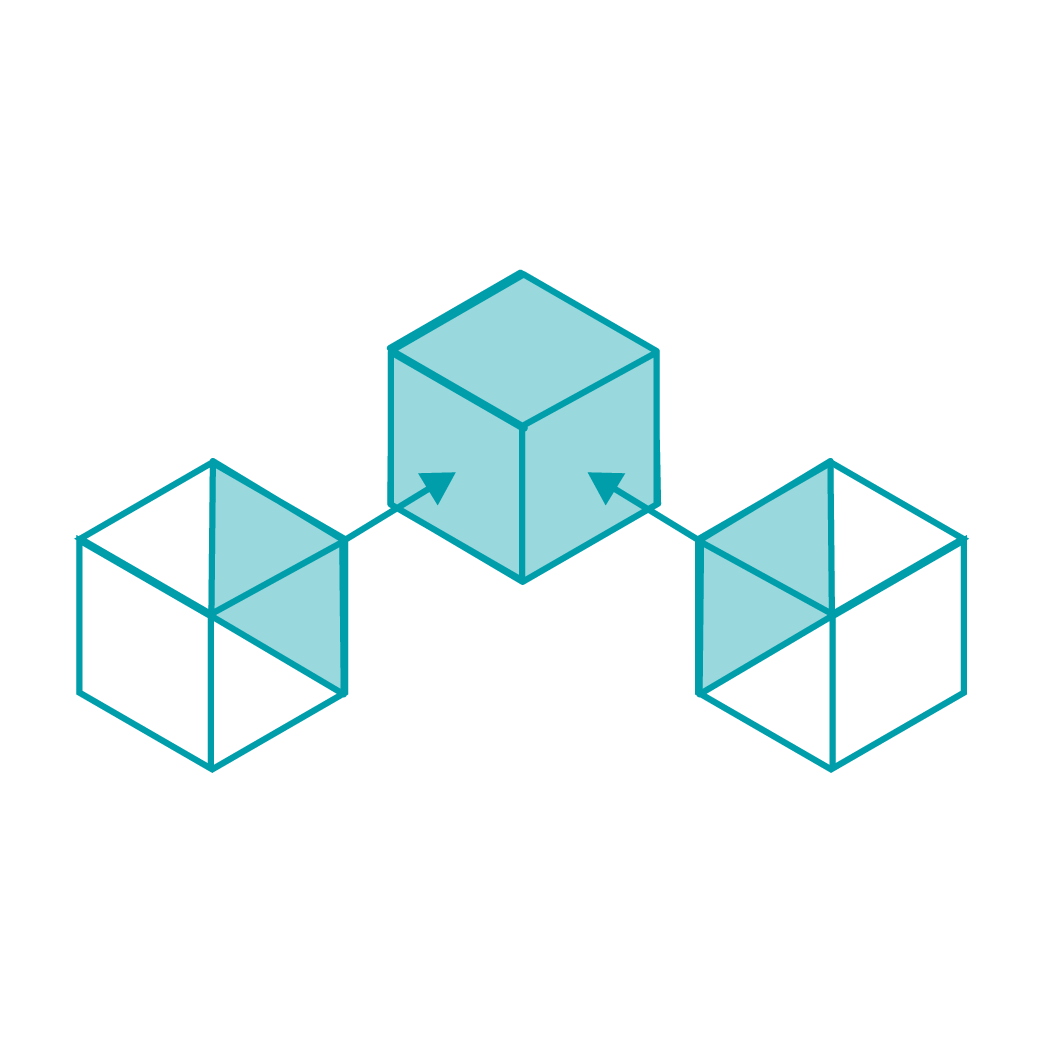

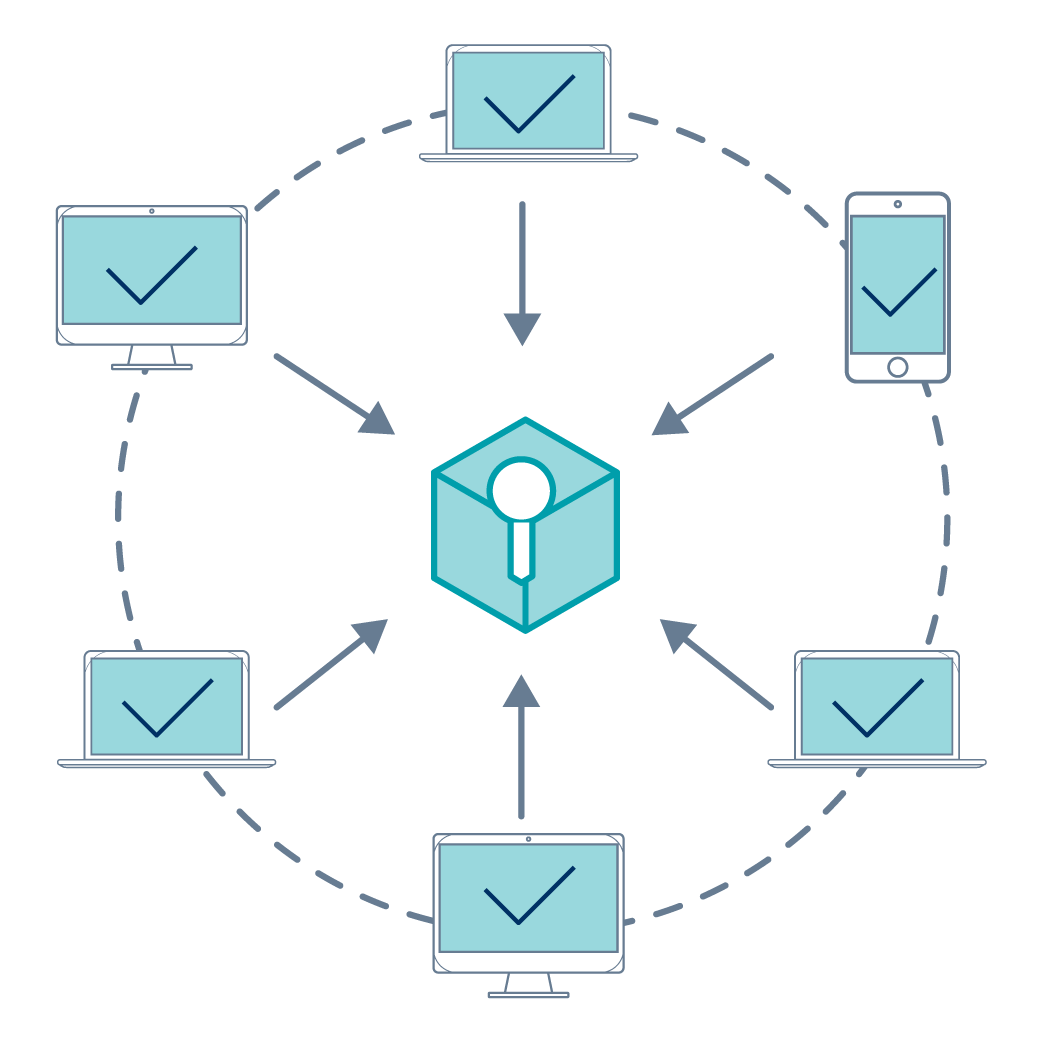

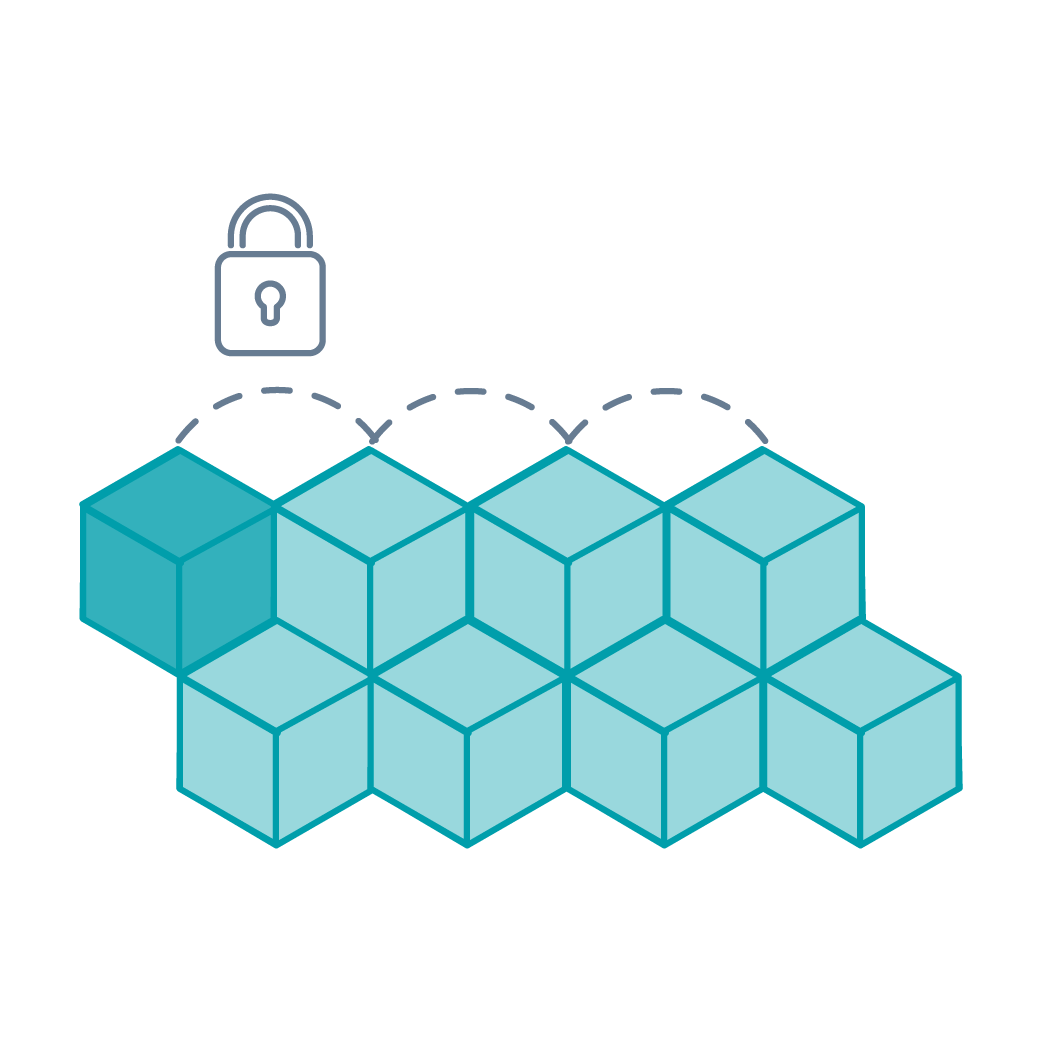

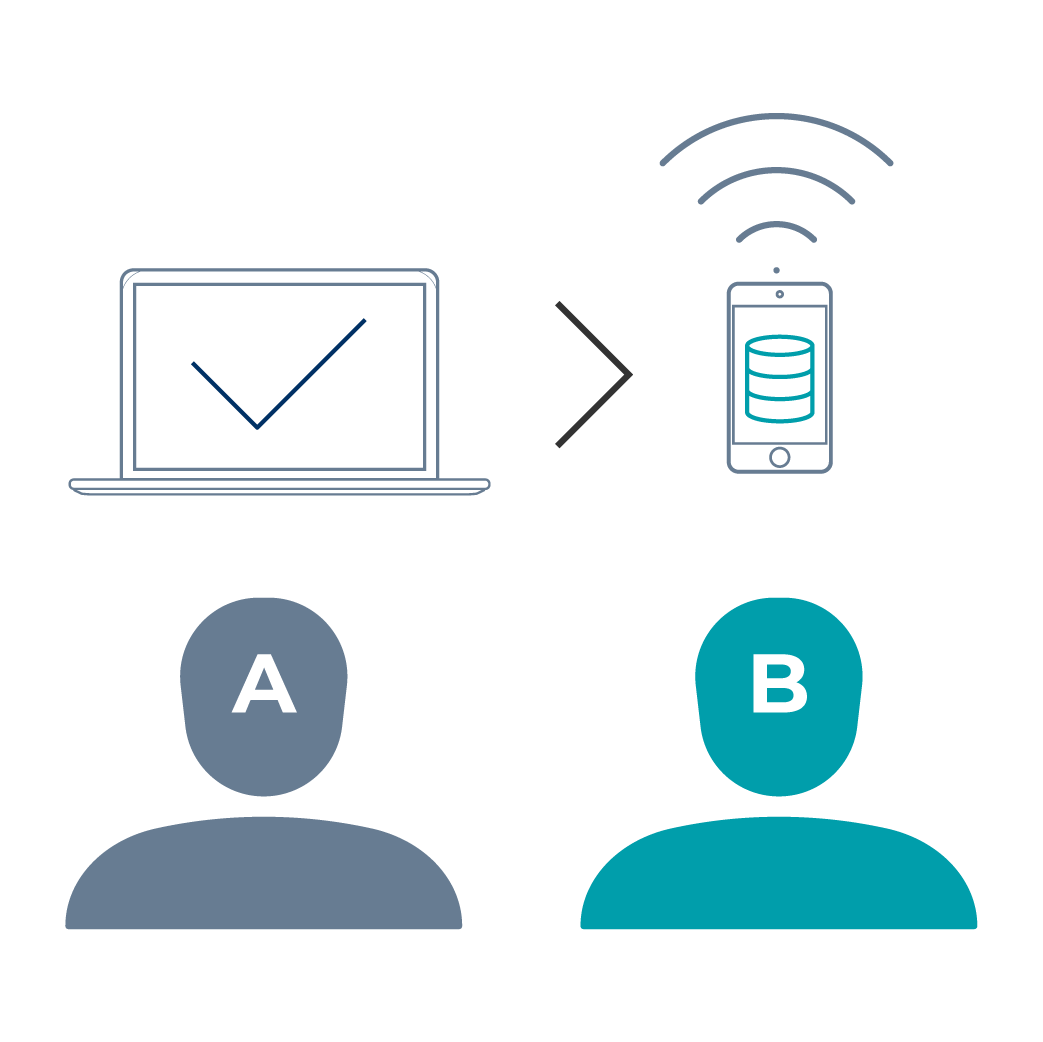

1

A transaction is requested

2

The transaction is broadcast to every party in the network

3

Those in the network approve the transaction as valid

4

The transaction is unified with other transactions as a block of data

5

The new block is added to the blockchain in a transparent and unalterable way

6

The transaction is complete

1

1A transaction is requested

2

2The transaction is broadcast to every party in the network

3

3Those in the network approve the transaction as valid

4

4The transaction is unified with other transactions as a block of data

5

5The new block is added to the blockchain in a transparent and unalterable way

6

6The transaction is completed

Development tools

Development tools Healthcare

Healthcare Supply chains

Supply chains

DeFi

DeFi Institutional platforms & services

Institutional platforms & services Insurance

Insurance Real estate

Real estate Trading & exchanges

Trading & exchanges

Data & analytics

Data & analytics Digital identity & privacy

Digital identity & privacy Hardware

Hardware RegTech

RegTech Smart contracts & DOAs

Smart contracts & DOAs

Art & collectibles

Art & collectibles Gaming & entertainment

Gaming & entertainment Trading platforms & exchanges

Trading platforms & exchanges Metaverse

Metaverse