Search

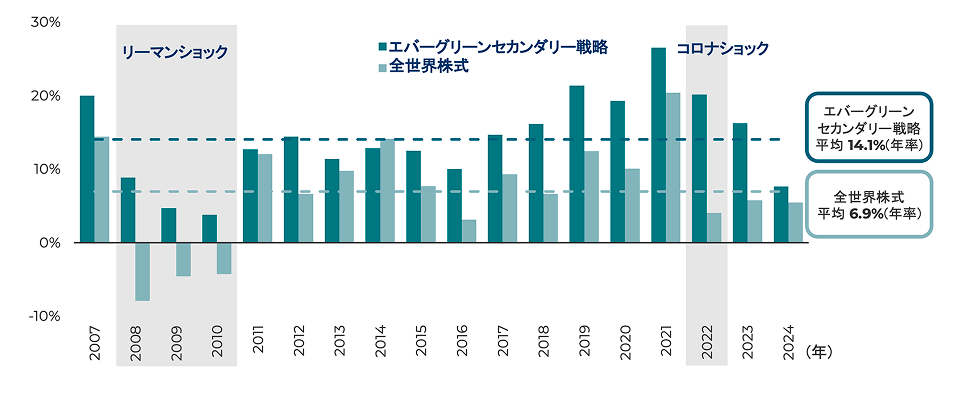

過去20年間にわたり一度もマイナスにならず、力強いリターンを創出

(1) 2025年3月末。出所:ハーバーベスト。 モデル化されたトラックレコードを示しています。過去の運用実績は将来の成果を保証するものではありません。本グラフに含まれる前提条件に関する追加の開示事項については、免責事項(1)をご参照ください。

ハーバーベスト・エバーグリーンセカンダリー戦略は、全世界株式と比べて力強くかつ下値抵抗力のある安定したリスク・リターンを投資家に届けることが期待されます。過去20年間、当社エバーグリーンセカンダリー戦略は、3年ローリングリターン(年率)ベースで一度もマイナスになったことはありません。

過去20年間にわたり一度もマイナスにならず、力強いリターンを創出

ハーバーベストのクローズエンド型セカンダリー戦略は、1991年以降の11ファンドにおいて、一度も元本割れになったことはありません。これは、リーマンショックやコロナショックといった相場変動時においても、下値抵抗力があることを示しております(2) 。セカンダリー投資は、市場動向に左右されにくい、オールウェザー型の戦略となります。

(2) 2025年6月末。出所: ハーバーベスト。

(3) 最終的なアロケーションは、経済環境および適切な投資機会の有無に左右されます。

(4) 2024年12月末。出所: Preqin。 グローバルにおけるセカンダリー、バイアウト、ベンチャー各戦略の元本割れファンド比率(TVPIが1倍未満のファンド比率)を記載。これは ハーバーベストのいかなるファンドまたはアカウントを代表するものではありません。過去の運用実績は将来の成果を保証するものではありません。本比較は説明目的のために提供されています。

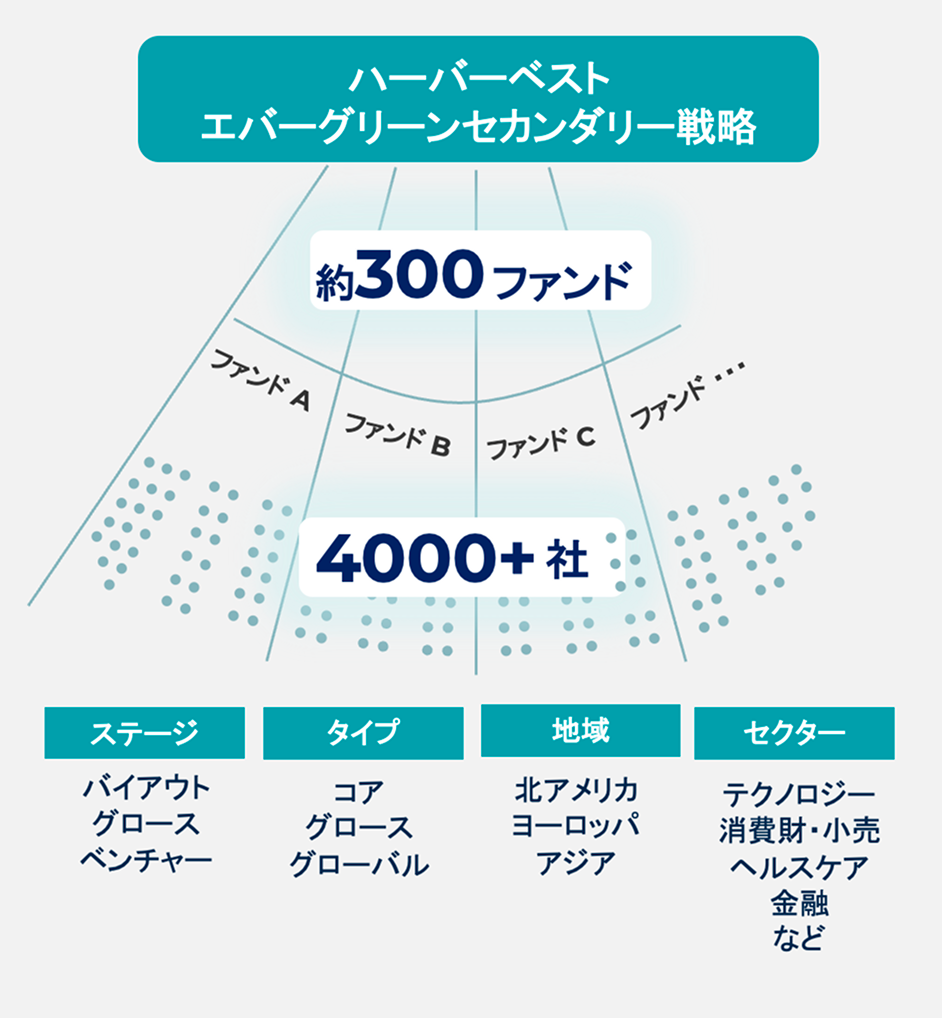

分散投資はセカンダリー投資の大きな魅力です。単一のプライベートエクイティ運用会社(GP)によって運用される一般的なPEファンドとは異なり、セカンダリーファンドは幅広い分散効果をご提供します。当戦略は約300ファンド、4000社超への投資を見込み、一般的なPEファンドとのあわせ持ちにも有効な選択肢となります。

セカンダリー投資を通じ、当戦略はステージ、タイプ、地域、セクターにわたり分散し投資を行います。

セカンダリーファンド全体では元本割れになったケースはわずか1.6%であり、バイアウトの13.1%とベンチャーの21.2%と比較して大幅に低い水準となっています。(4)

(1) 本モデルは、2025年3月31日時点のデータに基づき、90%をセカンダリー投資、10%をキャッシュ配分と仮定しています。モデル化された戦略のトラックレコードはグロスベースで提示されており、実際の投資家のリターンは手数料や費用の適用後には低くなります。なお、モデル化された戦略のトラックレコードは、対象となるジェネラルパートナーの手数料・費用を控除したネットベースですが、HarbourVestの手数料や費用(HSEC Luxの手数料・費用を含む)を控除していません。したがって、これはHSEC Luxの過去のパフォーマンスをシミュレーションしたものではありません。記載されたリターンを実際に受け取った投資家はいません。過去の実績は将来の結果を保証するものではありません。

MSCI AC World Net(USD)のパフォーマンスは2025年3月31日時点のものです(出典:Bloomberg)。MSCI AC World Net指数は、モデル化されたグロス戦略トラックレコードと同様に源泉税の取り扱いが近いため、比較目的で使用されています。グレーで表示された期間は、2025年1月30日時点のFRED(米国連邦準備制度)によるGDPベースの景気後退期を示します。

本情報は参考目的のみであり、投資の管理や意思決定に依拠すべきではありません。過去のパフォーマンスは将来の結果を示すものではありません。

上記のモデル情報は仮定に基づくものであり、説明目的のみです。モデル化されたリターンは参考情報としてのみ使用されるべきであり、投資判断に依拠すべきではありません。このトラックレコードは、HarbourVestのセカンダリープラットフォームにおける投資の等加重ポートフォリオの過去実績を示すことを目的としています。将来のパフォーマンスは保証されず、経済状況や適切な投資機会の有無に依存します。モデルパフォーマンスの結果には本質的な制約があり、将来の結果を示す信頼できる指標とはみなされません。これはESMAマーケティングコミュニケーションガイドラインにおけるファンドパフォーマンスのシミュレーションを意味するものではありません。

分散投資は利益を保証するものではなく、損失を防ぐものでもありません。

(2) セカンダリープライベートエクイティのトラックレコードに基づきます。損失率は、1.0倍未満のTV/Fとなったすべての取引(実現済みおよび未実現)の累積損失額を、当該ポートフォリオ内のすべての取引に対する総資金提供額で割ったものです。過去のパフォーマンスは将来の結果を示すものではありません。

本資料は適格投資家向けのマーケティングコミュニケーションです。最終的な投資判断を行う前に、必ず目論見書をご参照ください。本情報や投資判断について疑問がある場合は、資格を有する金融アドバイザーにご相談ください。本資料には機密性の高い専有情報が含まれており、HarbourVestの書面による明示的な同意なしに配布・開示することはできません。

HarbourVest Partners, LLC は、1940年投資顧問法に基づく登録投資顧問です。本資料は情報提供のみを目的としており、特定の有価証券の売買や投資戦略の採用を勧誘または推奨するものではありません。また、過去または現在の投資推奨を示唆するものでもありません。本資料に示される見解は、作成時点における著者の誠実な意見であり、最終的な投資助言を構成するものではなく、そのまま依拠すべきものではありません。本資料はHarbourVestが独自に作成したもの、または信頼できると判断した情報源から取得したものですが、その正確性、十分性、完全性をHarbourVestが保証するものではありません。記載された出来事や予測が実際に起こる保証はなく、実際の結果は本書に示された意見と大きく異なる可能性があります。本資料に含まれる情報(金融市場のパフォーマンスに関する予測を含む)は、現時点の市場環境に基づいており、市場の変動や将来の事象等により変更または無効となる可能性があります。本資料に含まれる情報は厳重に機密扱いとし、HarbourVestの書面による明示的な承認なしに、いかなる形式でも複製または再配布してはなりません。

本資料のいかなる部分も、勧誘、申込み、推奨、適合性の表示、法的・税務上の助言、またはいかなる有価証券または投資の承認を意図したものではなく、またそのように解釈されるべきではありません。HarbourVestのファンドまたはその他の投資を評価・判断する際に、本資料の内容のみに依拠するべきではありません。

プライベート・マーケットへの投資は高いリスクを伴うものであり、そのような投資に伴うリスクを評価し、かつそれを負担できる能力を有する投資家のみが行うべきです。以下は、プライベート・マーケット投資に関する主なリスクの一部を要約したものです。

プライベート・マーケット・ファンドの構造および条件に関連するリスク

ファンド・オブ・ファンズ構造への投資は、投資家が直接プライベート・エクイティ・ファンドに投資する場合には生じない追加的なリスクを伴う可能性があります。これらのリスクには、(i) 複数階層の費用発生、(ii) 第三者運用者への依存、などが含まれます。

また、ファンドはキャピタルコールを行う場合があり、これに応じられない場合、投資の全損失を含む重大な不利益を被る可能性があります。

持分の流動性の欠如・譲渡制限・市場の不存在

プライベート・マーケット・ファンドまたはアカウントの投資家は、一般的にファンドのゼネラル・パートナーの承諾なしに持分を譲渡することはできません。さらに、クローズドエンド・ファンドの運用契約に定められた制限や、適用される証券法上の制限により、譲渡性が制約されます。したがって、投資家は資金を長期間拘束する覚悟が必要であり、ファンドの期間が14年以上に及ぶ場合もあります。また、プライベート・エクイティ・クローズドエンド・ファンドから投資家が途中で離脱できるケースは極めて稀です。投資資金の全損失の可能性があるため、その損失に耐え得る投資家のみが参加すべきです。

損失リスク

戦略の運用が必ずしも利益をもたらす保証はなく、損失を回避できる保証もありません。また、運用キャッシュフローがリミテッド・パートナーへの分配に充てられる保証もありません。戦略によっては部分的または全額の損失が発生する可能性があり、その損失を十分に負担できない投資家は投資すべきではありません。

レバレッジの使用

本戦略ではレバレッジ(借入やデリバティブなど)を利用する場合があります。これには、オプション、先物、フォワード契約、スワップ、レポ取引など、元来レバレッジ特性を持つ手段を含みます。レバレッジの使用により、市場エクスポージャーおよびリスクが大幅に増大する可能性があります。

“Professional Investor” under the Securities and Futures Ordinance (Cap. 571 of the Laws of Hong Kong) (the “SFO”) and its subsidiary legislation) means:

(a) any recognised exchange company, recognised clearing house, recognised exchange controller or recognised investor compensation company, or any person authorised to provide automated trading services under section 95(2) of the SFO;

(b) any intermediary, or any other person carrying on the business of the provision of investment services and regulated under the law of any place outside Hong Kong;

(c) any authorized financial institution, or any bank which is not an authorised financial institution but is regulated under the law of any place outside Hong Kong;

(d) any insurer authorized under the Insurance Ordinance (Cap. 41 of the Laws of Hong Kong), or any other person carrying on insurance business and regulated under the law of any place outside Hong Kong;

(e) any scheme which-

(i) is a collective investment scheme authorised under section 104 of the SFO; or

(ii) is similarly constituted under the law of any place outside Hong Kong and, if it is regulated under the law of such place, is permitted to be operated under the law of such place,

or any person by whom any such scheme is operated;

(f) any registered scheme as defined in section 2(1) of the Mandatory Provident Fund Schemes Ordinance (Cap. 485 of the Laws of Hong Kong), or its constituent fund as defined in section 2 of the Mandatory Provident Fund Schemes (General) Regulation (Cap. 485A of the Laws of Hong Kong), or any person who, in relation to any such registered scheme, is an approved trustee or service provider as defined in section 2(1) of that Ordinance or who is an investment manager of any such registered scheme or constituent fund;

(g) any scheme which-

(i) is a registered scheme as defined in section 2(1) of the Occupational Retirement Schemes Ordinance (Cap. 426 of the Laws of Hong Kong); or

(ii) is an offshore scheme as defined in section 2(1) of that Ordinance and, if it is regulated under the law of the place in which it is domiciled, is permitted to be operated under the law of such place,

or any person who, in relation to any such scheme, is an administrator as defined in section 2(1) of that Ordinance;

(h) any government (other than a municipal government authority), any institution which performs the functions of a central bank, or any multilateral agency;

(i) except for the purposes of Schedule 5 to the SFO, any corporation which is-

(i) a wholly owned subsidiary of-

(A) an intermediary, or any other person carrying on the business of the provision of investment services and regulated under the law of any place outside Hong Kong; or

(B) an authorized financial institution, or any bank which is not an authorised financial institution but is regulated under the law of any place outside Hong Kong;

(ii) a holding company which holds all the issued share capital of-

(A) an intermediary, or any other person carrying on the business of the provision of investment services and regulated under the law of any place outside Hong Kong; or

(B) an authorized financial institution, or any bank which is not an authorised financial institution but is regulated under the law of any place outside Hong Kong; or

(iii) any other wholly owned subsidiary of a holding company referred to in subparagraph (ii); or

(j) any person of a class which is prescribed by rules made under section 397 of the SFO for the purposes of this paragraph as within the meaning of this definition for the purposes of the provisions of the SFO, or to the extent that it is prescribed by rules so made as within the meaning of this definition for the purposes of any provision of the SFO.

The first of such classes of additional “professional investor”, under the Securities and Futures (Professional Investor) Rules (Cap. 571D of the Laws of Hong Kong), are:

(k) any trust corporation (registered under Part VIII of the Trustee Ordinance (Cap. 29 of the Laws of Hong Kong) or the equivalent overseas) having been entrusted under the trust or trusts of which it acts as a trustee with total assets of not less than HK$40 million or its equivalent in any foreign currency at the relevant date (see below) or-

(i) as stated in the most recent audited financial statement prepared-

(A) in respect of the trust corporation; and

(B) within 16 months before the relevant date;

(ii) as ascertained by referring to one or more audited financial statements, each being the most recent audited financial statement, prepared-

(A) in respect of the trust or any of the trust; and

(B) within 16 months before the relevant date; or

(iii) as ascertained by referring to one or more custodian (see below) statements issued to the trust corporation-

(A) in respect of the trust or any of the trusts; and

(B) within 12 months before the relevant date;

(l) any individual, either alone or with any of his associates (the spouse or any child) on a joint account, having a portfolio (see below) of not less than HK$8 million or its equivalent in any foreign currency at the relevant date or-

(i) as stated in a certificate issued by an auditor or a certified public accountant of the individual within 12 months before the relevant date; or

(ii) as ascertained by referring to one or more custodian statements issued to the individual (either alone or with the associate) within 12 months before the relevant date;

(m) any corporation or partnership having-

(i) a portfolio of not less than HK$8 million or its equivalent in any foreign currency; or

(ii) total assets of not less than HK$40 million or its equivalent in any foreign currency, at the relevant date, or as ascertained by referring to-

(iii) the most recent audited financial statement prepared-

(A) in respect of the corporation or partnership (as the case may be); and

(B) within 16 months before the relevant date; or

(iv) one or more custodian statements issued to the corporation or partnership (as the case may be) within 12 months before the relevant date; and

(n) any corporation the sole business of which is to hold investments and which at the relevant date is wholly owned by any one or more of the following persons-

(i) a trust corporation that falls within the description in paragraph (k);

(ii) an individual who, either alone or with any of his or her associates on a joint account, falls within the description in paragraph (k);

(iii) a corporation that falls within the description in paragraph (m);

(iv) a partnership that falls within the description in paragraph (m).

For the purposes of paragraphs (k) to (n) above:

An institutional investor as defined in Section 4A of the SFA and Securities and Futures (Classes of Investors) Regulations 2018 is:

(a) the Singapore Government;

(b) a statutory board as may be prescribed by regulations made under section 341 of the SFA, as prescribed in the Second Schedule of the Securities and Futures (Classes of Investors) Regulations 2018;

(c) an entity that is wholly and beneficially owned, whether directly or indirectly, by a central government of a country and whose principal activity is —

(i) to manage its own funds;

(ii) to manage the funds of the central government of that country (which may include the reserves of that central government and any pension or provident fund of that country); or

(iii) to manage the funds (which may include the reserves of that central government and any pension or provident fund of that country) of another entity that is wholly and beneficially owned, whether directly or indirectly, by the central government of that country;

(d) any entity —

(i) that is wholly and beneficially owned, whether directly or indirectly, by the central government of a country; and

(ii) whose funds are managed by an entity mentioned in sub‑paragraph (c);

(e) a bank that is licensed under the Banking Act 1970;

(f) a merchant bank that is licensed under the Banking Act 1970;

(g) a finance company that is licensed under the Finance Companies Act 1967;

(h) a company or co‑operative society that is licensed under the Insurance Act 1966 to carry on insurance business in Singapore;

(i) a company licensed under the Trust Companies Act 2005;

(j) a holder of a capital markets services licence;

(k) an approved exchange;

(l) a recognised market operator;

(m) an approved clearing house;

(n) a recognised clearing house;

(o) a licensed trade repository;

(p) a licensed foreign trade repository;

(q) an approved holding company;

(r) a Depository as defined in section 81SF of the SFA;

(s) a pension fund, or collective investment scheme, whether constituted in Singapore or elsewhere;

(t) a person (other than an individual) who carries on the business of dealing in bonds with accredited investors or expert investors;

(u) a designated market‑maker as defined in paragraph 1 of the Second Schedule to the Securities and Futures (Licensing and Conduct of Business) Regulations;

(v) a headquarters company or Finance and Treasury Centre which carries on a class of business involving fund management, where such business has been approved as a qualifying service in relation to that headquarters company or Finance and Treasury Centre under section 43D(2)(a) or 43E(2)(a) of the Income Tax Act 1947;

(w) a person who undertakes fund management activity (whether in Singapore or elsewhere) on behalf of not more than 30 qualified investors;

(x) a Service Company (as defined in regulation 2 of the Insurance (Lloyd’s Asia Scheme) Regulations) which carries on business as an agent of a member of Lloyd’s;

(y) a corporation the entire share capital of which is owned by an institutional investor or by persons all of whom are institutional investors;

(z) a partnership (other than a limited liability partnership within the meaning of the Limited Liability Partnerships Act 2005) in which each partner is an institutional investor.

An accredited investor as defined in Section 4A of the SFA and Securities and Futures (Classes of Investors) Regulations 2018 is:

(i) an individual —

(A) whose net personal assets exceed in value $2 million (or its equivalent in a foreign currency) or such other amount as the Authority may prescribe in place of the first amount;

(B) whose financial assets (net of any related liabilities) exceed in value $1 million (or its equivalent in a foreign currency) or such other amount as the Authority may prescribe in place of the first amount, where “financial asset” means —

(BA) a deposit as defined in section 4B of the Banking Act 1970;

(BB) an investment product as defined in section 2(1) of the Financial Advisers Act 2001; or

(BC) any other asset as may be prescribed by regulations made under section 341; or

(C) whose income in the preceding 12 months is not less than $300,000 (or its equivalent in a foreign currency) or such other amount as the Authority may prescribe in place of the first amount;

(ii) a corporation with net assets exceeding $10 million in value (or its equivalent in a foreign currency) or such other amount as the Authority may prescribe, in place of the first amount, as determined by —

(A) the most recent audited balance sheet of the corporation; or

(B) where the corporation is not required to prepare audited accounts regularly, a balance sheet of the corporation certified by the corporation as giving a true and fair view of the state of affairs of the corporation as of the date of the balance sheet, which date must be within the preceding 12 months;

(iii) A trustee of a trust which all the beneficiaries are accredited investors; or

(iv) A trustee of a trust which the subject matter exceeds S$10 million; or

(v) An entity (other than a corporation) with net assets exceeding S$10 million (or its equivalent in a foreign currency) in value. “Entity” includes an unincorporated association, a partnership and the government of any state, but does not include a trust; or

(vi) A partnership (other than a limited liability partnership) in which every partner is an accredited investor; or

(vii) A corporation which the entire share capital is owned by one or more persons, all of whom are accredited investors.

Continuation solutions encompass a host of transaction types in which a GP secures interim liquidity and/or additional primary capital for their LPs in a strongly performing asset, or set of assets, that the GP will continue to own and control. Specifically, they include continuation funds, new funds created by GPs for the purpose of acquiring the asset(s) that continue to be managed by the same GP and capitalized by one or several secondary buyers, or equity recapitalizations involving a direct equity or structured equity investment into a portfolio company. These transactions can also include a parallel investment from the GP’s latest fund into that same pool of assets (a “cross-fund trade”).