Principal,

Primary Product Specialist

Footnotes

- Source: MSCI Private Capital Solutions as of September 30, 2025. The Global Venture, Global Growth Equity, and Global Buyout (All Funds) return is a pooled fund IRR based on the cash flows of all Global Venture, Global Growth Equity, and Global Buyout funds in the benchmark. The Global Venture, Global Growth Equity, and Global Buyout Top Quartile return is a pooled fund IRR based on the cash flows for the Global Venture, Global Growth Equity, and Global Buyout funds in the benchmark that achieved upper quartile performance. Public market equivalent (MSCI AC World Total Return/ & S&P 500) also provided by MSCI Private Capital Solutions is based on a methodology of buying and selling the index with the same timing of cash flows as the All Funds return. The securities comprising the public market indices have substantially different characteristics than the private equity benchmarks, and the comparison is provided for illustrative purposes only. This industry data reflects the fees, carried interest, and other expenses of the funds included in the benchmark. Please note returns would be reduced by fees, carried interest, and other expenses borne by investors in a HarbourVest fund / account. Adjusted index returns to reflect a comparable public market equivalent (“PME”).

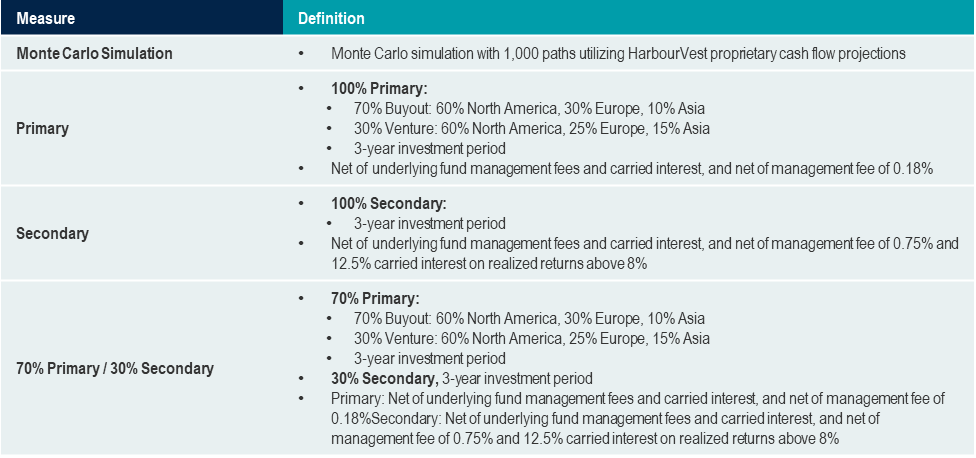

- The graphic and data shown in Figure 2 are based on a Monte Carlo simulation as of March 2026 leveraging HarbourVest’s proprietary dataset comprised of information aggregated from multiple data sources, including HarbourVest and third-party data providers. Not representative of any HarbourVest fund, account, and not representative of any HarbourVest experience. Returns are net of underlying fund fees and carry and are gross of any additional fees and expenses. Other expenses borne by investors in the HarbourVest managed funds / accounts may reduce returns. See Additional Important Information for important disclosures on Forward Looking Monte Carlo and Simulated Fee and Carry.

Assumptions for Figure 2:

- The graphic and data shown in Figure 3 are based on a forward-looking Monte Carlo simulation as of June 2025. Simulation Parameters: Co-investment: Vintage years for TVPI 2004 – 2018; Three-year investment period, 60% North America, 30% Europe, 10% Asia; 100% buyout. Returns are net of management fee of 1.0% and 12.5% carried interest on realized returns for third-party funds and gross of HarbourVest management fees and carried interest. Other expenses borne by investors in the HarbourVest managed funds / accounts may reduce returns. The Sortino ratio is a calculation of the expected return, or minimal acceptable return (MAR), divided by downside deviation, and similar to the Sharpe ratio, the higher the Sortino ratio the better. Sortino in this simulation assumes a minimum acceptable return (MAR/hurdle) of 1.5x for TVPI. Diversification does not ensure a profit or protect against a loss. Past performance is not a guarantee of future results.

- Source: MSCI Private Capital Solutions net LP pooled returns as of September 30, 2025, S&P Capital IQ. MSCI All Country World Index annual return as of the year indicated. Past performance is not a reliable indicator of future results. This is HarbourVest’s presentation of the data and is not responsible for the calculations conducted by HarbourVest, the formatting or configuration of this material, or for any inaccuracy in presentation thereof.

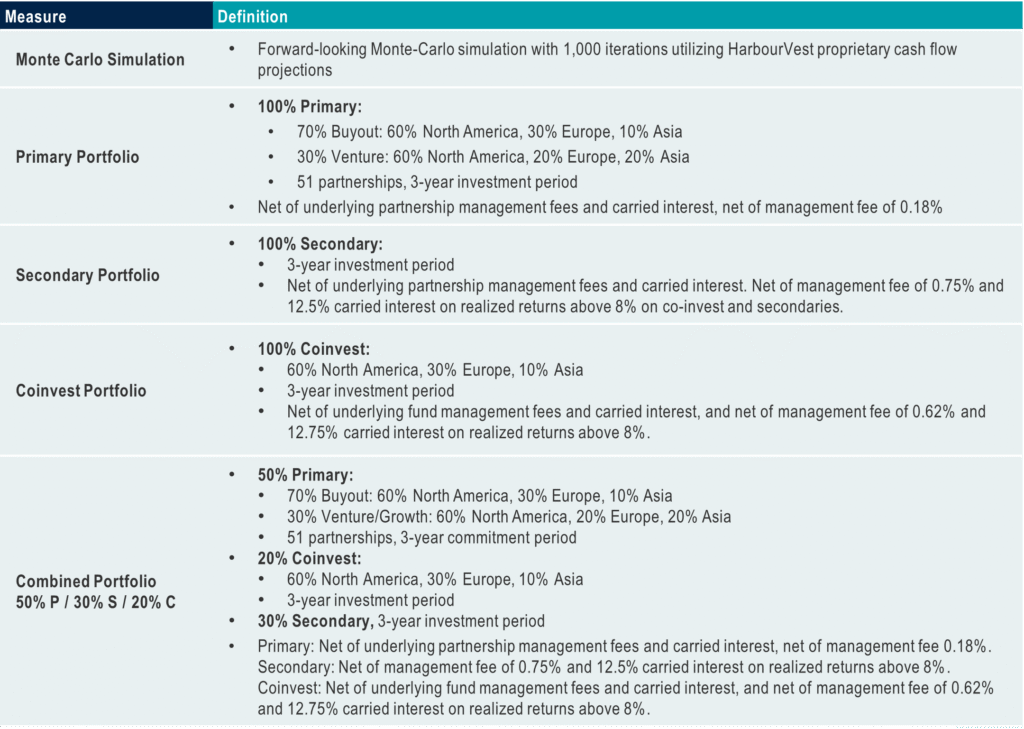

- The graphic and data shown in Figure 5 are based on a Forward-looking Monte Carlo simulation as of November 2024 leveraging HarbourVest’s proprietary data set comprised of information aggregated from multiple data sources, including HarbourVest and third-party data providers. Not representative of any HarbourVest fund, account, and not representative of any HarbourVest experience. Diversification does not ensure a profit or protect against a loss. Expected Surplus / Expected Shortfall / Sortino ratio assumes minimum acceptable return (MAR) of 8% for IRR and 1.5x for TVPI. Net of underlying management fees and carried interest. Secondary, co-investment, and combined portfolios are net of additional management fees and carried interest. Other expenses borne by investors in the HarbourVest managed funds / accounts may reduce returns. See ‘Additional Important Information’ for important disclosures related to Performance Returns, Fees and Expenses, Forward-looking Monte Carlo Simulations, and Simulated Fees and Expenses. Past performance is not a reliable indicator of future results.

Assumption for Figure 5

Disclosure

Important information

This material is solely for informational purposes and should not be viewed as a current or past recommendation or an offer to sell or the solicitation to buy securities or adopt any investment strategy. The opinions expressed herein represent the current, good faith views of the author(s) at the time of publication, are not definitive investment advice, and should not be relied upon as such. This material has been developed internally and/or obtained from sources believed to be reliable; however, HarbourVest does not guarantee the accuracy, adequacy or completeness of such information. There is no assurance that any events or projections will occur, and outcomes may be significantly different than the opinions shown here. This information, including any projections concerning financial market performance, is based on current market conditions, which will fluctuate and may be superseded by subsequent market events or for other reasons.

Market analysis is not representative of any HarbourVest product. This presentation contains quantitative analysis of the global private equity industry derived from HarbourVest’s proprietary Quant Database. The proprietary Quant Database is a compilation of private equity partnership and transactional data drawn from internal and external sources. The proprietary Quant Database has been developed internally based on information obtained from sources believed to be reliable; however, HarbourVest does not guarantee the accuracy, adequacy or completeness of such information. This proprietary database is intended to be representative of the broader private equity market and does not reflect the investment performance of any HarbourVest investment or the experience of any investor in any HarbourVest fund.

Market simulations are not representative of any investor’s experience. Simulated results based on the database will be impacted by an uneven representation of funds with different vintage years, sizes, managers, geographic investment focus, and strategies, and a limited pool of investment cash flow data. Capital call and distribution data are based on historic partnership investment cash flows, but do not represent the actual experience of any investor. The actual pace and timing of cash flows is likely to be different and will be highly dependent on the underlying partnerships’ commitment pace, the types of investments made by the fund(s), market conditions, and terms of any relevant management agreements. Market conditions have a significant impact on investments and could materially change the results. All simulations, projections, and pro forma results are based entirely on the output from numerous mathematical simulations. These simulations are unconstrained by the fund size, market opportunity, and minimum commitment amount, and do not take into account the practical aspects of raising and managing a fund. The simulated hypothetical results should be used solely as a reference to understand certain characteristics of private equity markets and should not be relied upon to manage investments or make investment decisions. Simulated market performance is not indicative of the future returns of any HarbourVest or third party fund or account, and there can be no assurance that future funds or accounts will achieve comparable results. Investments in private funds involve significant risks, including loss of the entire investment.

Simulation parameters are subject to change. This presentation contains model portfolios that represent HarbourVest’s current views on portfolio allocation intended to achieve the stated investment objectives. Such model portfolios are designed by HarbourVest personnel who are independent of HarbourVest’s investment teams; however, in constructing model portfolios, HarbourVest professionals may consider input from a variety of sources, including from internal investment professionals, who may have conflicts of interest related to the portfolio construction allocations. These portfolio construction assumptions inform certain market simulations shown herein. Portfolio construction assumptions should not be considered as investment advice or a recommendation of any particular strategy or investment product. Model portfolios presented herein are not tailored to address the investment objectives of any specific client. There is no guarantee that the model portfolio construction assumptions will work under all market conditions or will result in portfolios suitable for all investors. HarbourVest may change its view on portfolio allocations without notice and makes no representation that market simulations will be updated. No representation is being made that any model portfolio will or is likely to achieve profits, losses or results similar to those shown.

Additional important information

Diversification does not ensure a profit or protect against a loss.

HarbourVest Partners, LLC is a registered investment adviser under the Investment Advisers Act of 1940. This material is solely for informational purposes and should not be viewed as a current or past recommendation or an offer to sell or the solicitation to buy securities or adopt any investment strategy. The opinions expressed herein represent the current, good faith views of the author(s) at the time of publication, are not definitive investment advice, and should not be relied upon as such. This material has been developed internally and/or obtained from sources believed to be reliable; however, HarbourVest does not guarantee the accuracy, adequacy, or completeness of such information. There is no assurance that any events or projections will occur, and outcomes may be significantly different than the opinions shown here. This information, including any projections concerning financial market performance, is based on current market conditions, which will fluctuate and may be superseded by subsequent market events or for other reasons.The information contained herein must be kept strictly confidential and may not be reproduced or redistributed in any format without the express written approval of HarbourVest.

Nothing herein should be construed as a solicitation, offer, recommendation, representation of suitability, legal advice, tax advice, or endorsement of any security or investment and should not be relied upon by you in evaluating the merits of investing in HarbourVest funds or any other investment decision.

An investment in the private markets involves high degree of risk, and therefore, should be undertaken only by prospective investors capable of evaluating the risks of the Fund and bearing the risks such an investment represents. The following is a summary of only some of the risks of investing in private markets.

Risks Related to the Structure and Terms of a Private Markets Fund. Investments in a fund of funds structure may subject investors to additional risks which would not be incurred if such investor were investing directly in private equity funds. Such risks may include but are not limited to (i) multiple levels of expense; and (ii) reliance on third-party management. In addition, a fund may issue capital calls, and failure to meet the capital calls can result in consequences including, but not limited to, a total loss of investment.

Illiquidity of Interests; Limitations on Transfer; No Market for Interests. An investor in a HarbourVest-managed closed-end fund or account will generally not be permitted to transfer its interest without the consent of the general partner of such fund. Furthermore, the transferability of an interest will be subject to certain restrictions contained in the governing documents of a closed-end fund and will be affected by restrictions imposed under applicable securities laws. A HarbourVest-managed open-end fund or account will generally provide limited liquidity events for investors, subject to certain restrictions contained in the governing documents of an open-end fund and will be affected by restrictions imposed under applicable securities laws. There is currently no market for the interests in HarbourVest-managed funds or accounts, and it is not contemplated that one will develop. The interests should only be acquired by investors able to commit their funds for an indefinite period of time, as the term of the closed-end fund could continue for over 14 years. In addition, there are very few situations in which an investor may withdraw from a private equity closed-end fund. The possibility of total loss of an investment in a fund exists and prospective investors should not invest unless they can readily bear such a loss.

Risk of Loss. There can be no assurance that the operations of a strategy will be profitable or that the strategy will be able to avoid losses or that cash from operations will be available for distribution to the limited partners. The possibility of partial or total loss of capital of the strategy exists, and prospective investors should not subscribe unless they can readily bear the consequences of a complete loss of their investment.

Leverage. The strategy may use leverage in its investment strategy. Leverage may take the form of loans for borrowed money or derivative securities and instruments that are inherently leveraged, including options, futures, forward contracts, swaps and repurchase agreements. The strategy may use leverage to acquire, directly or indirectly, new investments. The use of leverage by the strategy can substantially increase the market exposure (and market risk) to which the strategies’ investment portfolio may be subject.

Availability of Suitable Investments. The business of identifying and structuring investments of the types contemplated by the strategy is competitive and involves a high degree of uncertainty. Furthermore, the availability of investment opportunities generally will be subject to market conditions and competition from other groups as well as, in some cases, the prevailing regulatory or political climate. Interest rates, general levels of economic activity, the price of securities and participation by other investors in the financial markets may affect the value and number of investments made by the strategy or considered for prospective investment.

Sustainable Investing. HarbourVest considers certain sustainable investing standards or metrics when evaluating investments as part of the larger goal of maximizing financial returns on investments. It should not be assumed that any sustainable investing initiatives, standards, or metrics utilized by HarbourVest will apply to each asset in which HarbourVest invests or that any sustainable investing initiatives, standards, or metrics were applicable to each of HarbourVest’s prior investments. Sustainable investing is only one of many considerations that HarbourVest takes into account when making investment decisions, and other considerations can be expected in certain circumstances to outweigh sustainable investing considerations. Any sustainable investing initiatives, standards or metrics will be implemented with respect to a portfolio investment solely to the extent HarbourVest determines such an initiative is consistent with its broader investment goals. Accordingly, certain investments may exhibit characteristics that are inconsistent with HarbourVest’s stated sustainability initiatives, standards, or metrics. Applying sustainable investing standards or metrics to investment decisions is qualitative and subjective by nature, and there is no guarantee that the criteria utilized by HarbourVest or any judgment exercised by HarbourVest in making an investment decision will reflect the sustainable investing-related beliefs or values of any particular investor or group of investors.

Reliance on the General Partner and Investment Manager. The success of the strategy will be highly dependent on the financial and managerial expertise of the Fund’s general partner and investment manager and their expertise in the relevant markets. The quality of results of the general partner and investment manager will depend on the quality of their personnel. There are risks that death, illness, disability, change in career or new employment of such personnel could adversely affect results of the strategy. The limited partners will not make decisions with respect to the acquisition, management, disposition or other realization of any investment, or other decisions regarding the strategies’ businesses and portfolio.

Market Risk. Private equity, as a form of equity capital, shares similar economic exposures as public equities. As such, investments in each can be expected to earn the equity risk premium, or compensation for assuming the non-diversifiable portion of equity risk. However, unlike public equity, private equity’s sensitivity to public markets is likely greatest during the late stages of the fund’s life because the level of equity markets around the time of portfolio company exits can negatively affect private equity realizations. Though private equity managers have the flexibility to potentially time portfolio company exits to complete transactions in more favorable market environments, there’s still the risk of capital loss from adverse financial conditions.

Incorporating artificial intelligence into the investment decision process. Recent technological advances in artificial intelligence and machine learning technology (collectively, “Machine Learning Technology”) and the reliance on Machine Learning Technology for investment and allocation decision making could pose risks to HarbourVest, the Fund and its portfolio companies or their respective affiliates. Machine Learning Technology is generally highly reliant on the collection and analysis of large amounts of data, and it may not be possible or practicable to incorporate all relevant data into any given model that Machine Learning Technology utilizes to operate. Additionally, certain data in such models will inevitably contain a degree of inaccuracy and error—potentially materially so—and could otherwise be inadequate or flawed, which would likely degrade the effectiveness of Machine Learning Technology. To the extent that HarbourVest, the Fund, or the portfolio companies utilize Machine Learning Technology and its applications, including in the private investment and financial sectors, continue to develop rapidly, and it is impossible to predict the future risks that may arise from such developments.

Potential Conflicts of Interest. The activities of the strategies may conflict with the activities of other HarbourVest-managed funds or accounts.

Tax Risks. An investment in the strategy involves tax risks, which may be material, including the risk of tax payments and tax filing obligations in multiple jurisdictions, which may apply both to the investor and the strategy. The taxation of the strategy and investors in the strategy is complex and subject to uncertainty. Prospective investors should consult with their tax, legal, and accounting advisers prior to making an investment in the strategy in light of their specific circumstances.

Secondary Investing Risk. Secondary market transactions may impose higher costs than other investments and may require a fund to assume contingent liabilities associated with events occurring prior to the Fund’s investment. The overall performance of an Underlying Portfolio Fund acquired through a secondary transaction will depend in large part on the purchase price paid. In addition, a fund will generally not have any ability to negotiate terms with respect to interests in Underlying Portfolio Funds invested in through secondary market transactions.

Direct Co-Invest Strategy Risks. Direct co-investments result in HarbourVest holding a minority equity interest in portfolio companies where HarbourVest does not expect to be able to protect its portfolio investments or to control or influence effectively the business or affairs of such entities. In such investments, HarbourVest will rely on the existing management and board of directors of such companies, which could include representatives of other financial investors with whom HarbourVest is not affiliated and whose interests could at times conflict with HarbourVest’s interests. Such investments involve additional risks not present in investments where HarbourVest has control, including the possibility that such other investors have financial difficulties resulting in a negative impact on such investments or take actions contrary to the investment objectives of HarbourVest. A portion of HarbourVest’s assets are expected to be invested outside of the United States. Non-US securities involve certain factors not typically associated with investing in US securities, including risks related to greater price volatility in and less liquidity of some non-US securities markets. This risk could be greater for investments made in developing or emerging markets.

Primary Investing Risk. An investment in leveraged buyouts of companies; such leveraged investments are inherently sensitive to declines in portfolio company revenues and increases in portfolio company expenses and to increases in interest rates. Investments in growth equity and venture capital investments; such investments involve a high degree of business and financial risk that can result in substantial losses. Investments in small-cap opportunities are subject to higher volatility and lower financial resources than large-cap investments. The markets for these securities are also less liquid than those for larger companies. Investments in portfolio companies involved in the technology industry which is challenged by various factors including rapidly changing market conditions, new competing products, changing consumer preferences, and short product life cycles. Secondary market transactions may impose higher costs than other investments and may require the assumption of contingent liabilities associated with events occurring prior to the investment. In addition, investments in secondary market transactions may be based on information that may be incomplete or inaccurate.

Index Definitions:

Bloomberg is the source of the index data contained or reflected in this material. MSCI, S&P, FTSE Russell, and JP Morgan are the owners of the index data contained or reflected in this material and all trademarks and copyrights related thereto. This is HarbourVest’s presentation of the data. Bloomberg, MSCI, S&P, FTSE Russell, and JP Morgan are not responsible for the calculations conducted by HarbourVest, the formatting or configuration of this material, or for any inaccuracy in presentation thereof.

The MSCI AC World® Index (ACWI) is designed to measure the performance of publicly-traded large and mid-capitalization equity securities in global developed and emerging markets. The MSCI ACWI Index is maintained by Morgan Stanley Capital International (“MSCI”) and has historically captured approximately 85% coverage of the free float-adjusted market capitalization of its publicly-traded global equity opportunity set.

The S&P 500® Index is designed to measure the performance of publicly-traded equity securities of the large capitalization sector of the US market and includes 500 large companies having common stock listed on eligible U.S. exchanges. The S&P 500 Index is maintained by Standard & Poors (“S&P”) and has historically captured approximately 80% coverage of available market capitalization of publicly-traded equities in the US market.

MSCI Private Capital Solutions (f.k.a. Burgiss Private Index Data) (unless otherwise indicated) reflects the fees, carried interest, and other expenses of the funds included in the benchmark. Please note that Fund returns would be reduced by the fees, carried interest, and other expenses borne by investors in the Fund. Such fees, carried interest, and other expenses may be higher or lower than those of the funds included in the benchmark. Certain information contained herein (the “Information”) is sourced from/copyright of MSCI Inc., MSCI ESG Research LLC, or their affiliates (“MSCI”), or information providers (together the “MSCI Parties”) and may have been used to calculate scores, signals, or other indicators. The Information is for internal use only and may not be reproduced or disseminated in whole or part without prior written permission. The Information may not be used for, nor does it constitute, an offer to buy or sell, or a promotion or recommendation of, any security, financial instrument or product, trading strategy, or index, nor should it be taken as an indication or guarantee of any future performance. Some funds may be based on or linked to MSCI indexes, and MSCI may be compensated based on the fund’s assets under management or other measures. MSCI has established an information barrier between index research and certain Information. None of the Information in and of itself can be used to determine which securities to buy or sell or when to buy or sell them. The Information is provided “as is” and the user assumes the entire risk of any use it may make or permit to be made of the Information. No MSCI Party warrants or guarantees the originality, accuracy and/or completeness of the Information and each expressly disclaims all express or implied warranties. No MSCI Party shall have any liability for any errors or omissions in connection with any Information herein, or any liability for any direct, indirect, special, punitive, consequential or any other damages (including lost profits) even if notified of the possibility of such damages.

PERFORMANCE INFORMATION

The source of certain performance information is HarbourVest. In considering the performance information contained herein, prospective investors should bear in mind that past performance is not a reliable indicator of future results, and there can be no assurance that an investment sponsored (or an account managed) by HarbourVest will achieve comparable results or be able to implement its investment strategy or meet its performance objectives. The funds that made these investments may have had different terms and investment objectives than those proposed or modeled herein.

Certain information included herein has been obtained from sources that HarbourVest believes to be reliable (including, without limitation, the data needed for the calculation of performance returns in respect of any investment shown herein), but the accuracy of such information cannot be guaranteed. Additionally, amounts contained in these materials are generally unaudited and may be flash or preliminary amounts reported. HarbourVest will also present certain information based on prior period reporting, adjusted for current period activity. Figures reported to HarbourVest may be adjusted for the purposes of determining the estimated fair value of such investment in accordance with HarbourVest’s valuation policy. Underlying investment data presented by HarbourVest herein is as of the date stated and may rely on best available data known by HarbourVest as of such date. For additional information please contact your HarbourVest representative.

The foregoing performance information includes realized and unrealized investments. Unrealized investments are valued by HarbourVest in accordance with the valuation guidelines contained in the applicable partnership agreement. Actual realized returns on unrealized investments will depend on, among other factors, future operating results, the value of the assets and market conditions at the time of disposition, any related transaction costs, and the timing and manner of sale, all of which may differ from the assumptions on which the valuations used in prior performance data contained herein are based. Accordingly, the actual realized returns on these unrealized investments may differ materially from returns indicated herein.

Certain performance in this presentation is calculated based on the experience of investors taking into account the effect of subscription credit facilities and similar financing. The use of subscription credit facilities and other financing allows the fund to acquire investments before or after the dates on which capital is contributed by and distributed to investors and may also be used to facilitate transactions involving the recapitalization of portfolio investments. This can shorten the period of time used to calculate the internal rate of return (IRR) actually received by investors, which results in a higher IRR for investments than the IRR that would result if the dates of investments by the fund had been used. This leveraging effect is generally more pronounced in funds with shorter operating histories. The firm’s funds routinely use fund-level subscription facilities in their investment strategies. Fund-level subscription facilities are defined as, “any subscription facilities, subscription line financing, capital call facilities, capital commitment facilities, bridge lines, or other indebtedness incurred by the private fund that is secured by the unfunded capital commitments of the private fund’s investors.” As applicable, NAV loan facilities held at the fund level are secured by NAV. For example, an investment into a fund that doubles in value over a 6 year holding period produces an illustrative IRR of 12.25% without the effect of leverage, but if a fund delays calling investor capital for 12 months through the use of a subscription credit facility, investors in the fund would experience an illustrative IRR of 14.87% from the same investment, before accounting for expenses of the credit facility.

To the extent that expenses of the credit facility do not fully offset this leveraging effect, IRRs experienced by investors and presented herein will be higher than IRRs experienced by the fund. Please contact HarbourVest if you have any questions regarding our investment performance or calculation methodologies.

Performance is expressed in US dollars, unless otherwise noted. Returns do not include the effect of any withholding taxes. Cash flows are converted to US dollars at historic daily exchange rates, unless otherwise indicated. The return to investors whose local currency is not the US dollar may increase or decrease as a result of currency fluctuations.

Historical Monte Carlo Simulations: These model (hypothetical) portfolios, if shown, are intended for illustrative purposes only. Performance information for each hypothetical portfolio utilized a Monte Carlo Simulation and are based on the actual cash flows of a proprietary data set that includes partnership investments made by Funds, along with partnership data from external sources. The capital calls and distribution data is based on historic partnership investment cash flows, but does not represent the actual experience of any investor or Fund. The results of the simulation are impacted by an uneven representation of funds with different vintage years, sizes, managers, and strategies, and a limited pool of investment cash flow data. The actual pace and timing of cash flows is likely to be different and will be highly dependent on the underlying partnerships’ commitment pace, the types of investments made by the Fund(s), market conditions, and terms of any relevant management agreements. The results presented are hypothetical and based entirely on the output from numerous mathematical simulations. The simulations are unconstrained by the fund size, market opportunity, and minimum commitment amount, and do not take into account the practical aspects of raising and managing a fund. The simulated hypothetical portfolio results should be used solely as a guide and should not be relied upon to manage your investments or make investment decisions. Simulation parameters are subject to change. There is no guarantee any simulation or its parameters will be updated.

Forward Looking Monte Carlo Simulations: The information presented herein is intended for illustrative purposes only. Performance and cash flow information are forecasted utilizing a Monte Carlo Simulation which incorporates forward looking market parameters calibrated using an industry level historical dataset. The performance information does not represent the actual experience of any investor or Fund. The results of the simulation are impacted by the composition of the historical dataset, which may include an uneven representation of funds with different vintage years, sizes, managers, and strategies, and a limited pool of investment cash flow data. The actual pace and timing of cash flows is likely to be different and will be highly dependent on the underlying partnerships’ commitment pace, the types of investments made by the Fund(s), market conditions, and terms of any relevant management agreements. The results presented are hypothetical and based entirely on the output from numerous mathematical simulations. The simulations are unconstrained by the fund size, market opportunity, and minimum commitment amount, and do not take into account the practical aspects of raising and managing a fund. The simulated hypothetical portfolio results should be used solely as a guide and should not be relied upon to manage your investments or make investment decisions. Simulation parameters are subject to change. There is no guarantee any simulation or its parameters will be updated.

Simulated Management Fee and Carry: The simulated performance presented herein is hypothetical and does not reflect any actual fees or expenses experienced by a client or investor. Instead, the simulated performance utilizes model management fees and carry that are assumed for modeling purposes only and applied as described below. No actual client or investor attained the performance presented here. Management fees are calculated either based on committed or invested capital and applied to portfolio’s gross capital calls according to a specified fee rate and a fee term. Carry is accrued based on a specified carry rate and applied to a portfolio’s total value after the applicable carry hurdle rate is met. Accrued carry is applied to gross NAV. Carry starts being distributed (paid out of distributions) once committed capital has been returned to investors.

Country Disclosures

European Economic Area

This information shall not constitute an offer or solicitation in relation to any HarbourVest fund (“Fund”) or any investment services provided by HarbourVest or its affiliates in any jurisdiction, or to any person, to whom it is unlawful to make offer or solicitation. In relation to each member state of the EEA (each a “Member State”) which has implemented Alternative Investment Fund Managers Directive (Directive (2011/61/EU)) (the “AIFMD”) (and for which transitional arrangements are not/no longer available), this document may only be distributed to the extent that: (1) the Fund is notified for marketing or pre-marketing to professional investors in the relevant Member State in accordance with AIFMD (as implemented into the local law/regulation of the relevant Member State); or (2) this document may otherwise be lawfully distributed and the Fund may otherwise be lawfully offered or placed in that Member State (including at the initiative of the investor). If the AIFM decides to terminate its arrangement for marketing the Fund in any EEA country where it is registered for sale, the AIFM will do so in accordance with the relevant AIFMD rules.

United Kingdom

This information shall not constitute an offer or solicitation in relation to any HarbourVest fund (“Fund”) or any investment services provided by HarbourVest or its affiliates in any jurisdiction, or to any person, to whom it is unlawful to make an offer or solicitation. This communication may only be distributed and the Fund may only be offered or placed in the United Kingdom to the extent that: (1) the Fund is permitted to be marketed to “professional investors” in the United Kingdom in accordance with the Alternative Investment Fund Managers Directive (Directive 2011/61/EU), as implemented into the local law/regulation of the United Kingdom; or (2) this communication may otherwise be lawfully distributed and the Fund may otherwise be lawfully offered or placed in the United Kingdom (including at the initiative of the investor).

This communication is issued in the United Kingdom by HarbourVest Partners (U.K.) Limited, 2nd Floor, 20 Air Street, London, W1B 5AN(registered in England and Wales (number 2512083), and authorised and regulated by the Financial Conduct Authority in the United Kingdom (FCA Reference Number: 147086) to, and/or is directed only at, persons who are professional clients or eligible counterparties for the purposes of the FCA’s Conduct of Business Sourcebook. The opportunity to invest in the Fund is only available to such persons in the United Kingdom and this communication must not be relied or acted upon by any other persons in the United Kingdom. This communication does not contain investment advice and the information included in it should not be considered as a recommendation to purchase, hold or sell any particular security, financial instrument or specified investment.

Switzerland

HarbourVest funds (the “Fund”) will exclusively be distributed to qualified investors (the “Qualified Investors”), as defined in Article 10(3) and (3ter) of the Swiss Collective Investment Schemes Act (“CISA”) and its implementing ordinance. The Fund is not registered with Swiss Financial Market Supervisory Authority (“FINMA”). In respects to offering or marketing the Fund in Switzerland to Qualified Investors with an opting-out pursuant to Art. 5(1) of the Swiss Federal Act on Financial Services(“FinSA”) and without any portfolio management or advisory relationship with a financial intermediary pursuant to Article 10(3ter) CISA, the Fund has appointed a Swiss Representative and Paying Agent. The Representative of the Fund in Switzerland is ACOLIN Fund Services AG, Maintower, Thurgauerstrasse 36/38, 8050 Zürich. The Paying Agent of the Fund is Banque Cantonale de Genève, 17 Quai de l’Ile, CH-1211 Geneva 2, Switzerland. The place of performance for interests of the Fund offered or distributed in or from Switzerland is the registered office of the Representative. Copies of the Private Placement Memorandum, Limited Partnership Agreement, and annual and semi-annual reports of the Fund can be obtained free of charge from the Representative.

For further information for Prospective and Existing Investors in Switzerland, please refer to Other Regulatory Disclosures

Abu Dhabi Global Market (“ADGM”)

This material is distributed in the ADGM to prospective investors by HarbourVest Partners (GCC) Limited which is duly licensed and regulated by the ADGM Financial Services Regulatory Authority (the “FSRA”). This material and related financial products or services are intended only for “Professional Clients” as defined under the FSRA rules, or any other such local equivalent where applicable and must not, therefore, be delivered to, or relied on by any other type of person.

This material and associated materials are provided to prospective investors for their exclusive use. This material is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution would be unlawful under the applicable laws of such jurisdiction. Any distribution, by whatever means, of this document and related material to persons other than those referred to above is strictly prohibited.

The FSRA accepts no responsibility for reviewing or verifying any Private Placement Memorandum, Prospectus or other documents, including this material in connection with this Fund. The FSRA has not approved this material or any other associated documents nor taken any steps to verify the information set out in this document and has no responsibility for it .The interests or shares are illiquid and subject to significant restrictions on their resale. Prospective investors should conduct their own due diligence on the interests or shares. If prospective investors do not understand the contents of this material, prospective investors should consult an authorized financial advisor.

This material is not intended for Retail Clients.

For additional legal and regulatory information related to other HarbourVest offices and countries please refer to:

https://www.harbourvest.com/important-office-and-country-disclosures/